Whether you're moving across town or across the country, I'm here to help. From finding your ideal neighborhood to connecting you with the best local resources, we specialize in making your relocation easy and stress-free.

Buying a home typically requires a variety of forms, reports, disclosures, and other legal and financial documents. A knowledgeable real estate agent will know what's required in your market, helping you avoid delays and costly mistakes. Also, there's a lot of jargon involved in a real estate transaction; you want to work with a professional who can speak the language.

A great real estate agent will guide you through the home search with an unbiased eye, helping you meet your buying objectives while staying within your budget. Agents are also a great source when you have questions about local amenities, utilities, zoning rules, contractors, and more.

You want access to the full range of opportunities. Using a cooperative system called the multiple listing service, your agent can help you evaluate all active listings that meet your criteria, alert you to listings soon to come on the market, and provide data on recent sales. Your agent can also save you time by helping you winnow away properties that are still appearing on public sites but are no longer on the market.

There are many factors up for discussion in any real estate transaction-from price to repairs to possession date. A real estate professional who's representing you will look at the transaction from your perspective, belping you negotiate a purchase agreement that meets your needs and allows you to do due diligence before you're bound to the purchase.

Most people buy only a few homes in a lifetime, usually with quite a few years between purchases. Even if you've bought a home before, laws and regulations change. Real estate practitioners may handle hundreds or thousands of transactions over the course of their career.

A home is so much more than four walls and a roof. And for most buyers, a home is the biggest purchase they'll ever make. Having a concerned, but objective, third party helps you stay focused on the issues most important to you when emotions threaten to sink an otherwise sound transaction.

When you're interviewing agents, ask if they're a REALTOR®, a member of the National Association of REALTORS®. Every member must adhere to the REALTOR® Code of Ethics, which is based on professionalism, serving the interests of clients, and protecting the public.

Below you will find the customary distribution of expenses for the purchase of real estate in Texas. Keep in mind that many of these items can be negotiated by either party at the time of the offer, excluding some expenses the lender requires the seller to pay.

Escrow fees

Document preperation (if applicable)

Recording changes for all documents related to the transfer of title to the buyer

Prorated share of taxes (from the date of acquistion)

All new loan charges and fees (except those the lender requires the seller to pay), including:

Appraisal, Credit report, Tax Service fee, Loan origination/discount fee, Reserves for taxes and insurance, Flood certification, Mortgage insurance premium

Title insurance premium: Lender's Policy

Interest on the new loan from the date of funding to 30 days prior to the first payment date

Inspection fees

Homeowner's transfer fee (if applicable)

Fire insurance premium for the first year

Real Estate Agent's commission (s)

Escrow fees

Payoff all loans in the seller's name (unless the existing loan balance is being assumed by the buyer), including: Interest accrued to the lender that is being paid off. Statement fees, release fees and any prepayment penalties.

Home warranty (according to contract terms)

Any judgements, tax liens, etc. against the seller

Prorated share of taxes (for any taxes unpaid ar the time of the transfer of title)

Any unpaid homeowners association dues

Recording charges to clear all documents of record against the seller

Any outstanding assessments

Any and all delinquent taxes

Title insurance premium: Owner's Policy

Seller credit for closing costs (according to contract terms)

• Pre-approval determines which loan program best fits your needs.

• You won't waste time considering homes you cannot afford.

• You are ready to write and present an offer on the home you really want when you find it.Your agent can give the seller a pre-approval letter on your behalf.

• If there are multiple offers on properties, pre-approval puts you in a much better negotiating position.

• You will know the amount needed for down payment and closing costs.

• If you are a first-time buyer, you may be able to qualify for a special first-time buyer program that could allow you to afford more home for your money.

• If you feel you would like and can afford a higher mortgage payment, other options may be available. Speak with your lender for more information.

• Lastly, peace of mind.

is a three-digit proxy representing the health of your full credit report.

is a holistic view of your credit showing detailed personal information about your current credit activity and how you've handled debt in the past. Both the report and score are typically sourced from one of the three credit bureaus: Experian, Equifax, or TransUnion.

Scoring models commonly range from 300 to 850. Each lender sets its own standards for what constitutes a good credit score. In general, scores fall along this structure:

•800-850= EXCELLENT

•740-799= VERY GOOD

•670-739= GOOD

•580-669= FAIR

•300-579= POOR

There are two main credit scoring models used by different lenders: FICO and VantageScore. However, lenders have a clear preference for FICO; its model is used in over 90% of U.S. lending decisions.

FICO Scores:

•10% New Credit

•15% Length of Credit History

•10% Credit Mix

•35% Payment History

•30% Amounts Owed

REALTORS®, real estate brokers, closing attorneys, buyers and sellers are targets for wire fraud and many have lost hundreds of thousands of dollars because they simply relied on wire instructions received via email.

A fraudster will hack into a participant's email account to obtain information about upcoming real estate transactions. After monitoring the account to determine the likely timing of a closing, the fraudster will send an email to the buyer pretending to be the escrow agent or another party to the transaction. The fraudulent email will contain new wiring instructions or routing information, and will request that the buyer send funds to the fraudulent account.

Obtain the phone number of your Real Estate Broker, REALTOR®, Closing Attorney (if applicable) and your Escrow Officer as soon as an escrow is opened.

Prior to wiring, call the phone number you wrote down from step #1 above to speak directly with your Escrow Officer to confirm wire instructions. If you receive a change in wiring instructions supposedly from us or your Escrow Officer, be suspicious as we rarely change our wiring instructions.

Before issuing a title policy, title companies check for defects by examining public records, including deeds, mortgages, wills, divorce decrees, court judgments, tax records, liens and plats. The title search determines who owns the property, what outstanding debts are against it and the condition of the title. If someone claims interest in the property, the title company will pay for any actual loss (up to the amount of coverage) and defend your title in court when:

Mistakes made in examining records

Forgery and undisclosed heirs

Liens for unpaid taxes or contractors

A deed or other document in your chain of title is invalid;

A lien against your title exists because a previous owner failed to pay either a mortgage or deed of trust, judgment, or a charge by a homeowner's association;

A lien exists for labor materials furnished by a contractor without your consent;

Leases, contracts or options on your land weren't recorded in the public records or disclosed to you;

A notary public error or someone failed to properly sign a document in your chain of title;

The title policy failed to disclose legal restrictions on how you can use your property;

An easement exists that isn't in public records and that you don't know about;

Other liens or encumbrances on your title exist but aren't listed in the policy exceptions.

Most lenders require borrowers to buy new loan title policies when refinancing. When the new loan pays off the existing loan, the old loan title policy is no longer in effect. A title company issues new policies in connection with new loans. Title companies must discount the premium if refinancing occurs within seven years of the original loan date. Your owner title policy remains in full force and effect after a refinance.

Most lending institutions won't loan money for a house or other property unless you provide a loan title policy.

This policy protects the lender's investment by paying the mortgage if a title defect voids the owner's/buyer's title. Investors who buy the new loan often require a loan title policy. When you buy a house, title companies also issue an owner's policy unless you reject it in writing. You don't have to buy an owner's policy. The owner's policy protects your title against the covered risk set out in the policy.

A Municipal Utility District, or "MUD", is a political subdivision of the State of Texas operated by apublicly elected Board of Directors, which is created to provide infrastructure and services such as water, sewer, and stormwater drainage in areas where city services are not available.

MUDs are a very common way in Texas for new communities to be developed in areas where city services are not yet available.

MUDs have contributed greatly to the affordability of new homes in Texas and to the state's dynamic growth rate.

MUDs are typically financed through the sale of revenue bonds, which are paid off by the taxes and user fees which are levied on residential and commercial property located in the MUD.

The MUD tax is included in the annual property tax bill received by homeowners. If your taxes are escrowed, the MUD tax will be part of your monthly payment.

No, the MUD tax only pays for the cost of installing and operating the infrastructure, such as providing clean water and disposing of wastewater. Your monthly usage fee is billed just like any other utility bill.

As a community grows, MUD tax rates typically decline, as operating and debt service costs are shared by more homeowners.

In some cases, such as when an area is annexed by a surrounding municipality, the MUD is dissolved.

For more information visit www.tceq.texas.gov

A Public Improvement District (PID) is a designated area where property owners pay a special assessment for improvements and services within that area. The services must benefit the PID area, and are supplemental to services already provided by the city. PID assessments are often used for improvements such as roads, utility relocation, water distribution and wastewater lines, drainage improvements, landscaping and improving parks.

A PID can provide funding for supplemental services and improvements to meet the needs of the community that could not otherwise be constructed or provided.

A PID may be initially funded through either cash or bonds. Bonds are issued based on the property's appraised value, as determined by property size and potential improvement to land value.

Paying PID assessments varies according to the respective PID. Some PID payments are collected by the County Tax Assessor with other property taxes. Other PIDs may designate a trustee to collect the PID payments.

Enhanced landscaping, Additional open space, Lakes and fountains, Improved city parks, Shade structures, Various recreational & pedestrian improvements

PID assessments end when the tax levied against a property (such as a home) is paid in full. PID assessments may be spread out over 20-40 years, or they may be paid in-full and up-front by the homeowner.

Here are some of the principal reasons to obtain and review a survey:

• To determine whether improvements (buildings, driveways, fences, utility lines, etc.) intended to be located on your property encroach into a neighbor's property, or vice versa.

• To mark the boundaries on the ground, so they are clear to observers standing on or near the property.

• To provide the evidence needed by the title insurer to delete certain standard exceptions to coverage and thereby provide "extended coverage" against off-record title matters (including matters that would be revealed by an accurate survey).

WHEN TO USE AN EXISTING SURVEY

The TREC (Texas Real Estate Commission) Contract was revised several years ago giving the option to sellers and buyers to use existing surveys when appropriate. Per the TREC contract, not only does the buyer have to accept the survey, but lenders and title companies must also approve and accept it. Survey affidavits assist in research and review. However, the best information comes from those who have been on the property, particularly prospective buyers and their REALTORS®.

To avoid costly delays, the following guidelines for using an existing survey are provided:

• Survey should be completely legible. It must have the property address, complete legal description, flood certification and the surveyor's signature and seal on the drawing.

• Survey must reflect all permanent improvements that are currently on the property, including pools, fences, spas, decks, and additional square footage. If the sellers have added permanent structures that are not shown on the survey, it is important to identify new improvements such as a pool, gazebo, fence, etc. when signing the survey affidavit. This notifies all parties that the survey provided is not an accurate rendering of the property as of the current date.

Almost always it is advisable to forego using an existing survey if improvements have been built since the time the initial survey work was performed. When an incorrect survey is delivered to the buyer and their agent, a new one should be requested. The title company and lender must be informed of the need for a new survey.

WHEN TO OBTAIN A NEW SURVEY

It is recommended that a purchaser obtain a new survey if one or more of the following conditions exist:

• A survey shows that all significant improvements currently located on the property do not exist or cannot be found.

• Surveys exist only for portions of the property, but the property as a whole exists of two or more parcels that are not platted and that are described by "metes and bounds", such that without a surveyor's interpretation of the legal descriptions, one cannot be certain of whether the parcels are contiguous, or whether there might exist a "gap" between, or overlap of, property boundaries.

Even when one or more of the foregoing conditions are present, a survey might not be necessary, and the purchaser might wish to bear the risk of proceeding without a survey; unless required by the lender.

While both are great protections to have, home insurance and home warranties offer different types of protection. Learn what each covers and why you should consider purchasing both. Owning a home is the one of the greatest investments you'll make in your life. Protecting your assets is not just smart—it's imperative. The best way to do this is to purchase both a homeowners insurance policy and a home warranty. Purchasing both will cover your home, belongings, appliances and system components in case they need replacement or repair. But understanding the differences between the two products and why you need them can be tricky.

A home insurance policy covers any accidental damage to your home and belongings due to theft, storms, fires, and some natural disasters. There are four primary areas covered under the policy: the interior and exterior of your home, personal property in case of theft, loss or damage, and general liability that can arise when a person is injured while on your property. A home insurance policy is usually mandatory, and a bank will generally require you to obtain one before issuing a mortgage on a home. A policy is renewed yearly. All home insurance policies require a deductible, which is what you'll pay when a claim is made. The policy will then take care of any

A home warranty is a service contract that provides for repair or replacement of your system components and appliances that fail due to age and standard wear and tear. For instance, components of your HVAC, electrical, and plumbing, kitchen appliances and washer/dryer are all typically covered under this warranty. You can also cover larger systems like your pool and spa. Home warranties typically have 12-month contract terms, and are not mandatory to obtain a mortgage. A home warranty is purely elective, but it's a smart purchase.

Homeowners insurance typically protects your home from things that might happen, like fires, theft or natural disasters. On the other hand, a home warranty helps protect your budget when covered components of home systems and appliances break down due to normal wear and tear.

Storm Damage, Fire Damage, Theft, Water Damage

Heating and Cooling Systems, Appliances, Electrical System,

Plumbing System

Verify all owner's/seller's names; make sure they are listed on your contract. If any changes have occurred in marital status, if a death has occurred, or if the property is vested in a trust, we will need to know in advance.

At the listing appointment, determine if the seller is a "foreign person", as defined by applicable law. If you believe the seller could be classified as a foreign person, notify your escrow officer and all parties to the contract. A foreign person requires certain IRS documentation with most of the obligation falling upon the buyer.

We are required to obtain the seller's loan payoff information. We will need the name and phone of the lender, the loan number, and the full social security number for each person on the loan.

If an existing survey is to be provided to the buyer by the seller per the contract, it must be accompanied with the Residential Real Property Affidavit (T47).

Failure to provide the affidavit with the existing survey could result in the seller paying for a new survey.

Valid, unexpired U.S. government issued photo ID is required for each person signing documents. A state issued driver's license, a military ID and/or a passport are acceptable forms of identification.

Tax liens, judgments, HOA liens, IRS liens, bankruptcy and other involuntary liens will be addressed and some could take an extended time to clear. It is important to have open lines of communication between the seller and the title company to clear any clouds on title.

All dates in the contract should be complete. The effective date is the catalyst for all requirements/conditions in the contract. Incomplete dates in the contract can lead to confusion and misunderstandings which could delay your closing and funding!

Agreed repairs must be completed in a timely fashion.

Completion of repairs specifically required by the contract is often a lender requirement to fund the loan. Lenders can require the appraiser to re-inspect the property prior to closing to certify the repairs were completed.

If the property is in a subdivision with a mandatory owners' association, pay special attention to the boxes and blanks on the HOA addendum indicating the party responsible for delivering the subdivision information, as well as the time frame required for delivery.

It is important to understand the process when contracting into a short sale or foreclosure. Even after the contract is signed, the current lienholder still requires the seller to go through a process before approving the sale.

Choosing your Real Estate Agent.

Choosing your lender (know about different types of mortgage loans and pre-qualification).

Selecting your home (determine the type, the price, and the location).

The Offer (once you have found the property, make a written offer through your real estate agent).

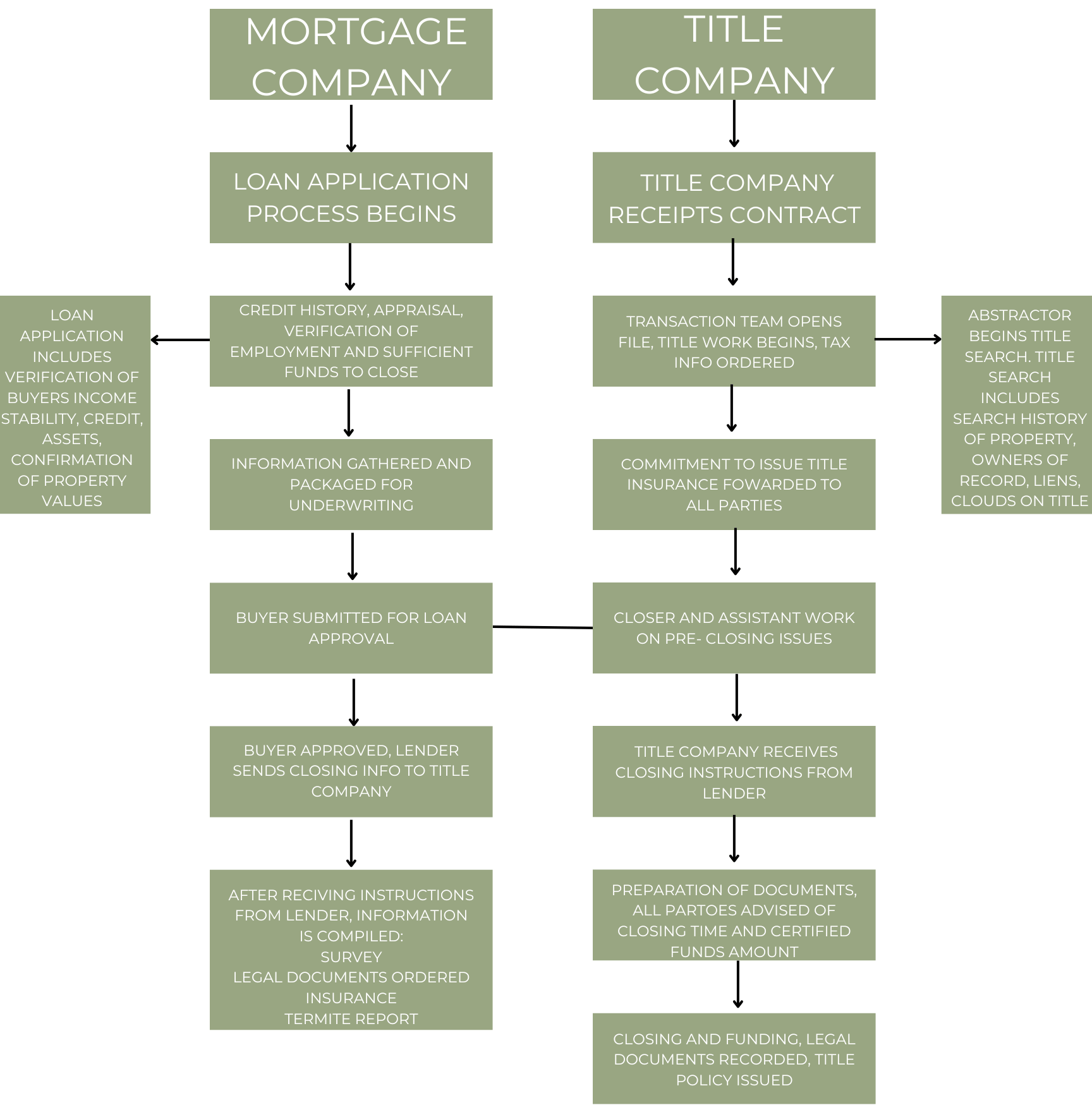

The escrow process (when you have reached an agreement with the seller, the initial good-faith deposit is given to a title company, and the process begins).

The mortgage loan (a mortgage loan is requested by filling out the application forms).

Preliminary title report (is reviewed and accepted).

Inspections and disclosures (the property is inspected during the period specified in the contract, and all disclosures made by the seller about the property are reviewed).

Appraisal (the property value is determined by the lender).

Loan approval (the lender contacts the escrow agent).

Homeowner's insurance (the buyer tells the title company the name of the insurance company that will grant the policy).

Conditions (the title company ensures the conditions are met).

Final visit to property (the buyer inspects the property with the Real Estate Agent, before closing the transaction.

Document signing (the buyer signs the loan documents, and deposits the closing costs and down payment with the title company).

The title company returns the documents to the lender.

The lender's funds are electronically transferred to the title company (the monetary exchange occurs between the lender and the title company).

The deed is registered at the county office by the title company (this transfers the property title to the buyer).

The transaction "funds" (accounting is finalized i.e. money is disbursed to all payees).

The keys are delivered to the new owner, and he takes possession of his new home.

Provide a fully executed contract of sale to the title company with the earnest money check.

Provide a copy of the contract of sale, receipted by the title company, to the mortgage company making your loan.

Call you loan officer and arrange to make formal loan applications.

If doing inspections of the home, schedule the appointment with the inspector and seller as soon as possible. A termite inspection may be required by the lender. Any bills to be paid at closing must be provided to the title company prior to closing.

Obtain homeowner's insurance. Supply information to the title company at least one week prior to closing.

If you want to review your loan documents prior to the closing, please request that your mortgage company provide the documents to the title company at least one day prior to closing so copies can be provided for your review.

If you will not be present at closing to sign documents and intend to use a Power of Attorney, the following must occur:

• The title company must approve the POA prior to closing.

• The original POA must be delivered to the title company before closing for recording with the County Clerk's office.

Valid drivers' license, passport or other government-issued picture identification

Send a wire transfer payment of funds at the time of closing. The title company must have your mortgage company's closing instructions to prepare the final closing figure. The complete closing package from the lender must be in the hands of the title company 24 hours prior to closing in order to meet the closing date deadline on the contract.

Bring any document requirements that your lender has requested you to produce at the closing table.

The original recorded Warranty Deed that transferred title of the property to you will be sent to you by the County Clerk's Office approximately one month after closing. Store this document for safe keeping for future reference. When the deed is recorded with the County Clerk's Office, your title becomes public record.

The Owner's Title Policy of the Title Insurance will be mailed to you approximately one month after closing.

This document should also be stored for safe keeping.

If you have not received the coupon book or other instructions about making your monthly mortgage payment, call your lender.

Make certain to file your homestead with the county appraisal district. You may file for property exemptions any time between January Ist and April 30th.

If your property taxes are being escrowed by your mortgage company, forward any original tax notices you may receive in the mail to your lender so that the taxes are paid in a timely manner.

It is the taxpayer's responsibility to be certain that the property is rendered in the taxpayer's name for the upcoming tax year. Contact the appraisal district for assistance in making certain this is done.

• Determine what you do and do not want to move - plan garage sale if necessary.

• Decide what you are going to pack yourself and what the movers are going to pack.

• Obtain boxes from your mover for items you will pack personally.

• Notify the post office of your new address.

• Gather medical and dental records for all family members.

• Call your utility service providers to arrange to transfer and set up utilities in your new home. Utilities may include cable and TV, internet, water and sewer, gas, electricity, satellite, security, trash and phone. You'll want to make sure you have working electricity and running water in your new home when you move in. Here are a few tips for transferring and/or setting up utilities:

• Create a list of all of your current utility providers and your new providers.

• Notify utility providers of your move a few weeks prior.

• Most water and sewer services will need to be arranged through your city.

• Check what (if any) utilities are handled by your HOA.

• Before moving, call all utility providers to confirm your stop/start dates.

• Study a floor plan and pictures of the home.

• It's a good idea to decide what will go where before the move, so you can instruct the movers where to place furniture and belongings. Try looking at a floor plan with measurements to see what will or won't fit inside a room.

• Clean the new house. Once you move, it's hard to do a deep clean of the house with boxes and furniture scattered about. So, before all of your items are unloaded into the house, hire a professional to do a deep clean of the home or do it yourself.

• Repaint the house and make improvements. If you plan to paint the interiors, it's best to do it before you move in. Otherwise, you'll have to move belongings and cover furniture - not to mention, fumes from the paint could give you a bad headache. If you plan to paint your home before moving in, remember first to clean the surfaces, repair cracks in the wall and tape off areas you don't want to paint.

• Turn on the AC or heating system in the new home. If it's hot outside, it's a good idea to turn the AC on inside the home before you move in to prevent mold and mildew. If it's cold out, you may want to turn the heat on before moving day, so you're not freezing inside the house.

POST-MOVE UNPACK NECESSITIES FIRST

From your toiletries to your kitchen gear, there are certain things you will need during the first week in your new home. Make sure that boxes filled with essentials are clearly labeled so you can find them when you need them. When unpacking your home, we recommend going room-by-room, starting with the bedrooms and the kitchen. Next, unpack your living room, office and laundry necessities. Save rooms with non-essentials, such as a gym, playroom and powder room, for last.

RECYCLE MOVING SUPPLIES

Finished unpacking? Now it's time to get rid of those boxes. You can always sell or give away moving boxes to those who need them, or you can simply take your moving supplies to the closest recycling center. Just don't forget to flatten the boxes before you go.

ORDER NEW FURNITURE & DECOR

After unpacking your belongings and arranging your furniture, you'll be able to better assess what you still need in the home. Whether it's a new corner sectional to fill the large living space or a few pieces of wall art to complete the room, now's the time to take stock of what you need.

CHANGE THE LOCKS

Don't forget to change the locks when you move in.

For safety and security reasons, making a few copies of the new keys is also a good idea in case you lose one. To rekey the house, you'll need to contact a local locksmith during the first week in your new home.

SET UP A SECURITY SYSTEM

If the home already has a security system in place, you'll need to contact the company to arrange for a transfer of service to your name. In addition, most security companies will want to come out to the house to make sure the security system is installed to your liking. Passwords and passcodes will also need to be changed.

GATHER ALL WARRANTY INFORMATION AND MANUALS

Often, former residents leave a folder with warranty information and appliance manuals for the new residents. After the move, locate this folder in your home. If you don't see one, reach out to the sellers (or their Realtor) to ask for warranty information if they have it.

TEST ALL SMOKE DETECTORS AND INSTALL CARBON MONOXIDE DETECTORS

Upon moving into your new home, test the smoke detectors to ensure they're in working order. Install carbon monoxide detectors on every level of the house. The EPA's directions for installing carbon monoxide detectors state: "Detectors should be placed on a wall about 5 feet above the floor. The detector may be placed on the ceiling. Do not place the detector right next to or over a fireplace or flame-producing appliance. Keep the detector out of the way of pets and children. Each floor needs a separate detector."

CHILD-PROOF THE HOME

If you have babies or small children, you know the importance of child-proofing a home as soon as possible. From stair gates and window locks to outlet covers and corner protectors, there are certain child-proofing tools you should include in either an easy-to-reach moving day bag or in a separate, clearly labeled box. Remember that simple precautions, such as closing bathroom doors, attaching doorknob covers and placing a toddler in a pack 'n play while unpacking, will go a long way in keeping your kids safe.

CALL A PEST CONTROL SERVICE PROVIDER

This company should offer quarterly inspections, spot treatments and same-day appointments when pest issues arise.

CONDUCT AN ENERGY AUDIT

For those that live in an older home and/or in a location with extreme temperatures (hey, Texas), it's important to conduct an energy audit of the new home. With an energy audit, a professional will conduct a room-by-room examination to detect any air leaks or gas leaks in the home. For instance, if cold air leaks through drafty windows, your HVAC system must work overtime to keep up with the home's heating needs. This leads to higher energy bills and wasted energy.

MAKE SURE MONTHLY PAYMENTS ARE AUTOMATED

It's easy to forget to pay certain bills (especially new bills) when you're busy unpacking and settling into a new home. Make it easier by automating all credit card and bill payments online. For instance, if the new home is part of an HOA community, you'll likely need to make monthly payments. To ensure you don't forget, go ahead and authorize automatic bill payments towards your HOA.

FIND A TRUSTED HANDYMAN, PLUMBER AND ELECTRICIAN

No matter where you move, you'll likely need a trusted handyman, plumber and electrician at some point. Don't wait until your AC dies or your toilet overflows to find one. Go ahead and research local service professionals in your area to figure out who you want to hire to help with home maintenance needs.

FIGURE OUT TRASH AND RECYCLING PICKUP DAYS

After purchasing your home, you can ask the sellers or neighbors for trash and recycling pickup timing.

Moving can be stressful for anyone, but it's also stressful for our furry friends. Pets have an instinctive fear of new surroundings, but as pet owners we can help them adjust quickly with careful planning and preparation. Here are some tips to help create a more pleasant experience for our pet companion (s).

PRE MOVE UPDATE TAG and microchips with new contact information. Make sure new collars fit snugly.

GET VET RECORDS and any prescriptions from your current vet so you can transfer them to your pet's new doctor.

TAKE TIME PACKING so as not to not stress out you or your pet. Bring moving boxes in early to help them

adjust to change.

DURING MOVE:

PACK ESSENTIALS such as medications, food, and toys. Make sure they are easy accessible.

SECURE IN CRATE or consider boarding your pet for the day to keep them safe.

REGULAR REST STOPS will help prevent accidents in the car. If traveling long distance research pet-friendly hotels in advance.

POST MOVE:

FIND A NEW VET immediately so you know where to go for emergencies.

LAY OUT ESSENTIALS START YOUR ROUTINE before unpacking your own things. This will give them some

so your pet can feel comfortable in their new home quickly.

Reduce your Real Estate Taxes

Under Texas law, a homebuyer may apply for the Homestead Tax Exemption in the same year that they purchase their home. It is no longer necessary to wait until January 1 of the following year before filing.

It is free to file for the Homestead Exemption. Once you receive the exemption, it generally remains in place; you do not need to reapply unless the chief appraiser in your district sends you a written notice asking you to reapply. For more information about timing, deadlines or requests to reapply, contact the Central Appraisal District for the county in which your property is located.

Use the list below to find your county and corresponding website.

For additional information, call your county appraisal district.

Collin County Central Appraisal District

Dallas County Central Appraisal District

Denton County Central Appraisal District

Ellis County Central Appraisal District

Fannin County Central Appraisal District

Grayson County Central Appraisal District

graysonappraisal.org / 903.893.9673

Hunt County Appraisal District

Johnson County Central Appraisal District

Kaufman County Central Appraisal District

kaufman-cad.org / 972.932.6081

Parker County Central Appraisal District

Rockwall County Central Appraisal District

rockwallcad.com / 972.771.2034

Tarrant County Central Appraisal District

Wise County Appraisal District

The Application for Homestead Exemption can also be found at https://comptroller.texas.gov/forms/50-114.pdf_

DEPRECIATION

Loss in value occasioned by ordinary wear and tear, destructive action of the elements, or functional or economic obsolescence.

AMORTIZATION

The paying off of an existing debt by regular partial payments.

APR

Annual Percentage Rate. The yearly interest percentage of a loan as expressed by the actual rate of interest paid.

BROKER

One who acts as an agent for another in negotiating sales or purchases in return for a fee or commission.

CHAIN OF TITLE

Beginning with a conveyance out of an original source of title such as a government, each succeeding deed, will, or other medium, which conveys and transfers the title to succeeding owners, constitutes a link in the chain of title. The chain of title is the composite of all such links.

CLOSING

In some areas called a "settlement." The process of completing a real estate transaction during which deeds, mortgages, leases and other required instruments are signed and/or delivered; an accounting between the parties is made, and the money is disbursed; the papers are recorded; and all other details such as payment of outstanding liens and transfer of hazard insurance policies are attended to.

CLOSING DISCLOSURE

The five-page Closing Disclosure must be provided to the consumer three business days before they close on the loan. The Closing Disclosure details all of the costs associated with their mortgage transaction.

CLOSING STATEMENT

A summation, in the form of a balance sheet, made at a closing, showing the debits and credits to which each party to a real estate transaction is entitled.

CLOUD ON TITLE

An irregularity, possible claim, or encumbrance which, if valid, would affect or impair the title.

CONTRACT

Same as "agreement," but usually more formal.

DEED

A written document by which title to real estate is conveyed from one party to another.

EARNEST MONEY

Down payment or a small part of the purchase price made by a purchaser as evidence of good faith.

ENDORSEMENT

Addition to or modification of a title insurance policy that expands or changes coverage of the policy, fulfilling specific requirements of the insured.

ESCROW

Technically, this term strictly refers to a deed delivered to a third person to be held by him until the fulfillment or performance of some act or condition by the grantee. In the title industry, it means depositing with an impartial third party anything pertaining to a real estate transaction, including money and documents of all kinds. The money and documents are to be disbursed and delivered to the rightful parties by the escrow agent or title company when all conditions of the transaction have been met.

ESCROW AGREEMENT

A written agreement usually made between buyer, seller and escrow agent, but sometimes only between one person and the escrow agent. It sets forth the conditions to be preformed incident to the object (usually money) deposited in escrow, and gives the escrow agent instructions.

EXAMINATION

In title industry terms, to peruse and study the instruments in a chain of title and to determine their effect and condition in order to reach a concluston. as to the title status.

EXAMINER

Usually referred to, in title industry terms, as the title examiner. One who examines and determines condition and status of real estate titles.

EXCEPTIONS

Insurance policies include a list of items excluded from coverage. Items excluded from coverage can be found in section two of Schedule B of the policy.

FORECLOSURE

A legal proceeding for the collection of real estate mortgages and other types of liens on real estate, which result in cutting off the right to redeem the mortgaged property and usually involve a judicial sale of the property.

GENERAL WARRANTY

A warranty provision in a deed or mortgage or other real estate instrument containing all of the common law items of warranty. Also known as a full warranty.

LIEN

The liability of real estate as security for payment of a debt. This liability may be created by contract, such as a mortgage, or by operation of law, such as a mechanics lien.

MORTGAGE

A temporary conditional pledge of property to a creditor as security for the payment of a debt that may be cancelled by payment.

OWNER'S POLICY

This policy is purchased for a one-time fee and protects a homeowner's investment in a property for as long as they or their heirs have an interest in the property.

POWER OF ATTORNEY

A legal instrument authorizing one to act as another's agent.

PREMIUM

The amount payable for an insurance policy.

PROBATE

A legal procedure in which the validity and probity of a document, such as a will, is proven.

PROMISSORY NOTE

A written promise to pay or repay a specified sum of money.

QUIT CLAIM DEED

Deed that does not imply the grantor holds title, but which surrenders and gives the grantee any possible interest or rights that the grantor may have in the property.

SETTLEMENT

In some areas called a "closing". The process of completing a real estate transaction during which deeds, mortgages, leases and other required instruments are signed and/or delivered; an accounting between the parties is made, and the money is disbursed; the papers are recorded; and all other details such as payment of outstanding liens and transfer of hazard insurance policies are attended to.

SPECIAL WARRANTY DEED

A deed that warrants the title only with respect to acts of the Grantor and the interests of anyone claiming, by, through, or under him.

SURVEY

The drawing by a surveyor that represents the property showing measurements, boundaries, area, and contours.

TITLE

(1) A combination of all the elements that constitute the highest legal right to own, possess, use, control, enjoy, and dispose of real estate or an inheritable right or interest therein. (2) The rights of ownership recognized and protected by the law.

TITLE COMMITMENT

An offer to issue a title insurance policy. The title commitment will describe the various conditions, exclusions and exceptions that will apply to that particular policy.

TITLE COVENANTS

Covenants ordinarily inserted in conveyances and in transfers of title to real estate for the purpose of giving protection to the purchaser against possible insufficiency of the title received. A group of such covenants known as

"common law covenants"

include: (a) covenants against encumbrances; (b) covenant for further assurance (in other words, to do whatever is necessary to rectify title deficiencies); (c) covenant of good right and authority to convey; (d) covenant of quiet enjoyment; (e) covenant of seisin;

(f) covenant of warranty.

TITLE DEFECT

(1) Any possible or patent claim or right outstanding in a chain of title that is adverse to the claim ownership. (2) Any material irregularity in the execution or effect of an instrument in the chain of title.

TITLE EXAMINATION

To peruse and study the instruments in a chain of title and to determine their effect and condition in order to reach a conclusion as to the status of the title.

TITLE INSURANCE

Insurance that protects purchasers of real estate and mortgages against loss from defective titles, liens and encumbrances.

TITLE PLANT

A geographically filed assemblage of title information which is to help in expediting title examinations, such as copies of previous attorneys' opinions, abstracts, tax searches, and copies or take-offs of the public records.

TITLE SEARCH

A search and perusal of the public records for recorded instruments that affect the title to a particular piece of land.

UNDERWRITER

An insurance company that issues insurance policies either to the public or to another insurer.

WARRANTY DEED

A deed containing one or more title covenants.